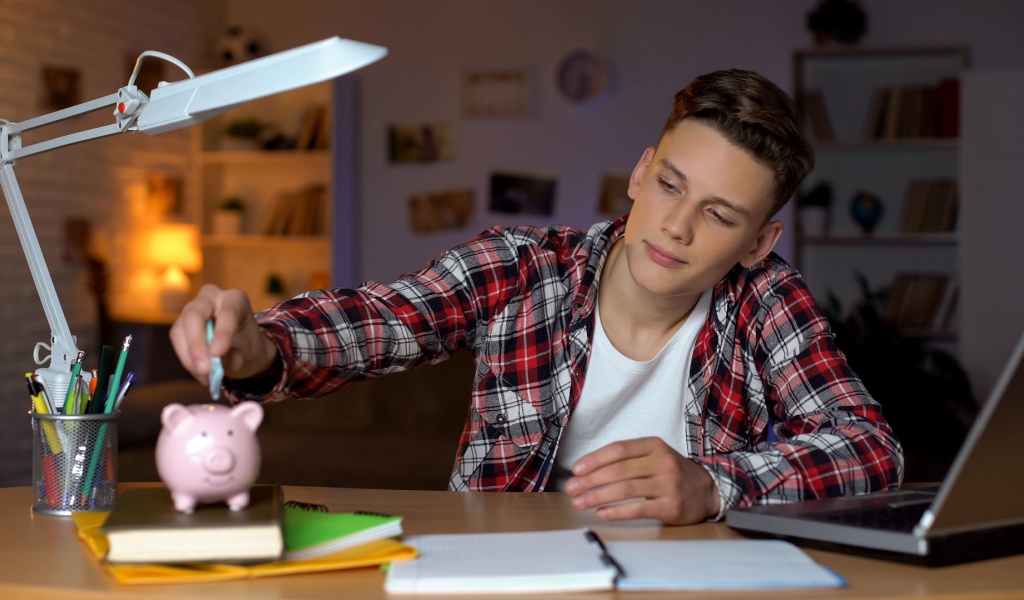

It may seem obvious but savings is actually one of the most ignored aspects of a budget, even with those who follow one religiously. People tend to think they will save whatever is “leftover” after expenses have been covered, but what do you know, there’s never any!

That’s why it’s much better to treat savings itself as an expense. Add it as a line item into your budget and the put the money away at the beginning of the month so you wouldn’t end up flaking. Savings should not be an afterthought, but something you consciously do to build yourself a better future.

Saving Isn’t Optional

Just like you wouldn’t treat the electricity fee or the house help as optional, savings shouldn’t be either. Any retired person will tell you how much they value the savings they made in their younger days (or bemoan the regret for not doing so). At the very least, saving can help you get out of an emergency without bankrupting yourself.

Unfortunately, most of us tend to focus on spending rather than saving when it comes to managing our finances. Savings are treated like a stray cat that wanders over to your backyard. Maybe if you had a fishbone leftover after your meals, you might feed it. But instead, it should be treated like a beloved house cat who is fed only the most premium of cat foods – or at least something from the discount pile at the pet store (hey, at least it’s getting fed!).

“Most individuals, if they don’t line-item savings in, they just spend whatever money they have at the end of the month, and most aren’t disciplined enough to actually put that [remaining money] into a retirement account,” says Jeff Weber, a certified financial planner with Titus Wealth Management in San Mateo, California.

A 401k is the exception to this reality, and that’s only because you are literally forced to save as the money is taken out of your paycheck and put away somewhere else. It’s like a firewall for impulse spending.

But a lot of people do not have an employer-mandated savings plan. In that case, you can set up short term savings accounts for goals like buying a new car or house, or long-term goals like a retirement account, and of course, the all-important rainy-day fund.

Make Saving a Line Item

Tracking spending is one of the first and most important steps of setting up and following a budget. You may use apps, spreadsheets, or sheer memory power to do this. While you’re ticking off things like rent, power, childcare fees, etc., savings should be in that list of non-negotiable payments as well.

Transfer the designated amount into your savings account even before you take care of expenses to ensure you don’t go overboard with your other expenses. This will condition your mind to treat

savings as a fixed expense like the others.

“It’s easy to talk about budgeting your money, but it takes discipline to follow through on those plans,” says Dara Luber, senior manager of retirement at TD Ameritrade.

Weber Says automatic transfers are a great way to do this. When it is made automatic, with little to no effort on your part, you don’t have to think about it and are less likely to change your mind on impulse. “I have my clients set up a separate account at a bank or brokerage — it is less likely that they’re going to spend that money.”

How Much Should You Save & Where to Put It

This is one of the biggest questions facing you once you decide to make saving a line item in your budget. Obviously, the percentage will vary depending on your income and lifestyle but 15% is a good place to start when it comes to your retirement fund. This is from your pre-tax income and would include things like 401(k) and IRA.

Employer contributions don’t need to be factored in, but Weber recommends counting the amount that is taken out of your paycheck, like your 401(k), as it helps you see the bigger picture. Other than this, you can section your savings into different categories like your children’s college fund or saving for a vacation later in the year.

As for where your money should go, it will depend on when you expect to make use of it. You can contribute to an IRA in addition to your 401k to make that next egg just a little bit bigger. Savings that you intend to make use of it’s the short term (5 years or less), can be held in a high-yield online savings account, but long-term savings could be better off invested in a taxable brokerage account.

The Added Benefit: Freedom to Spend

Many people think of a budget as restrictive and that they’ll never be able to spend on something fun again. But the reality is quite the opposite. Once you know that your money is being put to good use, you will feel content. Another plus is that since you know how all the money is to be used and that you’ve saved a good portion of it as well, you can spend whatever is leftover without an ounce of guilt!